Blog

ASSANTE MARKET UPDATE: MAKE VOLATILITY GREAT AGAIN

- by Adil Mohammed, CFP®, CIM®, FCSI®

- March 11, 2025

Assante Friends and Family,

Over the past few weeks, I’ve had several conversations with clients, friends and family who are understandably frustrated, annoyed and nervous about the recent tariff noise and are concerned about the potential implications. These conversations almost always end with some form of “Trump is such a…”

I’m not saying I disagree, but there’s more to the story. As a result, I thought this would be a good opportunity to provide some context about what’s going on in financial markets.

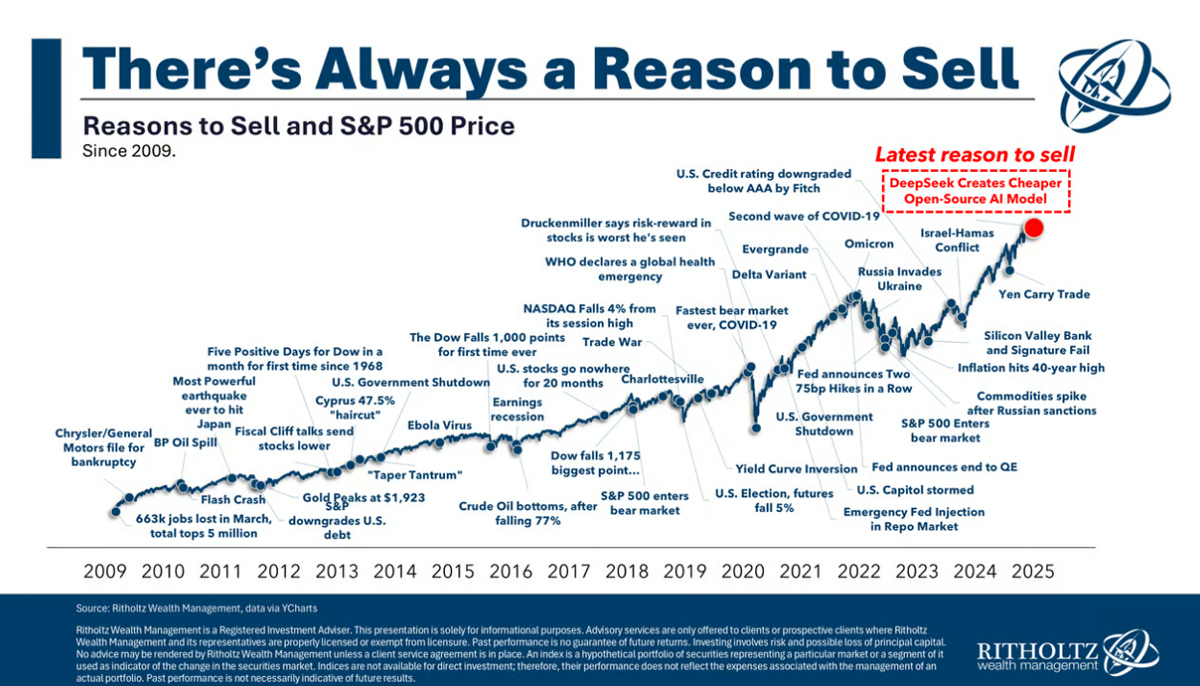

THIS IS NORMAL

Let me start by saying – market volatility is back.

Our blog post to start the year was titled “temper your expectations” highlighting the fact that we’ve experienced two extremely strong years of market returns with minimal volatility in 2024.

Combine this with high investor expectations coming into the year plus a change in the US administration means a market correction was expected.

This is something we’ve been telling investors to be prepared for since September – see here.

I know you’ve heard me say it again and again but it’s worth repeating – market volatility is normal, necessary, and part of the plan.

What’s not normal?

Receiving your last 5 quarterly statements in which the market value is higher than in the previous quarter. Or how about experiencing no major market fluctuations over the past 18 months?

That’s not normal.

You don’t get to see your statement go up forever, there must be a pullback.

Remember, volatility is not a bug in the system, it’s a feature.

A healthy market takes one step back, two steps forward.

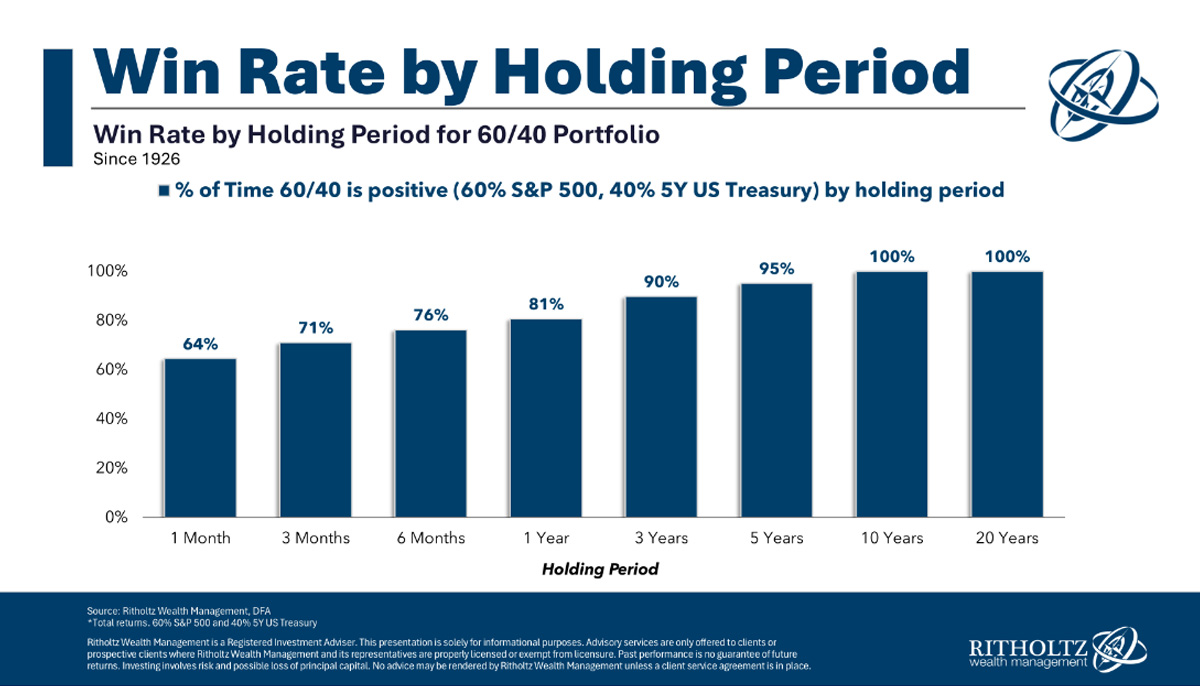

History says that in 64% of years, the market should experience a 10%+ correction.

If we want our 5%, 6%, 7%, or 8% + returns, the stomach-churning uncomfortableness is the price we pay to get there.

I know this one may feel different because it’s been a while but you’ve been through this before…

YOU’VE BEEN THROUGH THIS BEFORE

Don’t get me wrong it hasn’t been easy but you’ve seen this movie before…

- 2018 – 20% market drawdown

- 2020 – 34% market drawdown

- 2022 – 25% market drawdown

In the past 15 years you’ve experienced:

- Fourteen 5-10% market drawdowns

- Six 10-20% market corrections

- Two bear markets where stocks fell more than 20%

In the last 5 years, we’ve had a global pandemic, soaring inflation, a jump in interest rates, two wars and 5 bank failures.

How does the movie always end?

With markets continuing to climb higher regardless of the wall of worry.

IT’S NOT JUST TRUMP

So why are we experiencing this market correction?

Everyone wants to blame Trump and his trade war. Sure, that’s part of the story but not the whole story.

While his tariffs are certainly not helping, the US economy is slowing and has shown signs of slowing prior to serious tariff talk.

Whether you look at investor sentiment, consumer confidence, retail sales, the job market, specific company commentary (ex. Walmart), or GDP – many of the metrics that provided a tailwind in 2023 and 2024 – they are starting to slow.

That’s to be expected given their strong showing over the last 2 years.

However, the data has started to come in lower than expected and the fear is that this slowing could lead to a recession.

Up until the last few weeks, the market has tried to look beyond these risks, but these renewed recession fears combined with the official start of the Trump tariffs has proven to be too much.

IF IT WASN’T TRUMP, IT WOULD HAVE BEEN SOMETHING ELSE

I know it’s easy to blame Trump for the recent market turbulence but it’s worth mentioning that if it wasn’t Trump, something else would have caused a correction. It was just a matter of time.

We give far too much credit to politicians when the market is rising and place too much blame when the market is falling.

The fact is, there are many forces that play a more impactful role on the financial markets than politicians.

Typically it’s a multitude of factors when put together cause the market to rise or fall and in this case, the Trump policies are only part of the story.

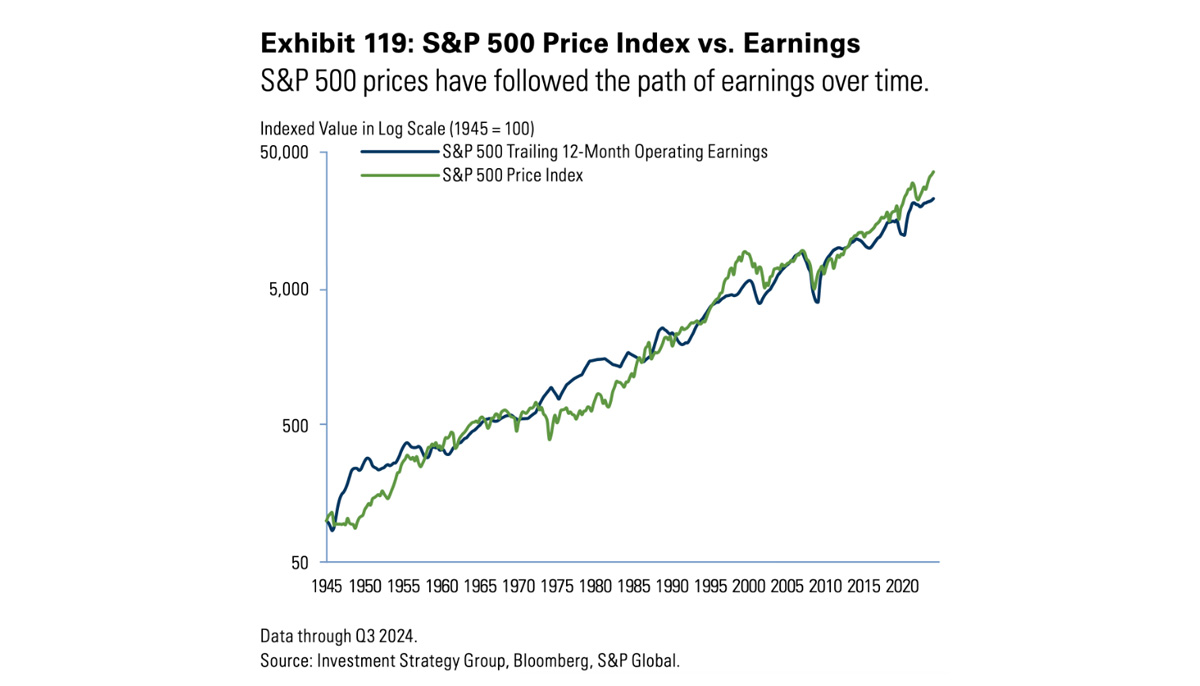

WHAT ACTUALLY MATTERS? COMPANY EARNINGS

Company earnings are what matters. I cannot stress this enough.

We are not investing in the economy or politics or in recessions and we’re not investing in tariffs.

Economic and geopolitical forces only matter to the degree that they affect company earnings.

Remember, we are investing in companies and more specifically in the profits of those companies, with the belief that those companies will continue to grow their profits over time.

The chart below shows the relationship between company earnings and market returns – they trend together.

If companies continue to earn more money over time, markets go up – simple as that.

Ask yourself if you think Apple will be around 5 years from now, or Walmart, or Costco or Visa? Do you think these companies will find a way to continue to earn more money?

The objective of the portfolio managers is to find companies that can continue to grow their earnings regardless of the market environment.

Sure there will be pullbacks and bumps along the way, but over time, if earnings are up, markets are up.

It’s important to point out that so far, much of this market pressure is coming from quantitative and factor driven funds, as well as tariffs and political headlines.

This means that computer algorithms (rather than humans) are doing a lot of the trading and when the selling hits a certain level, these algorithms are programmed to sell more.

It’s purely sentiment driven meaning there has been little to no changes to the fundamentals of the underlying companies.

In fact, earnings estimates have actually ticked higher.

In other words, these periods are tremendous buying opportunities for the portfolio managers to purchase the same great companies at a discount.

MARKET TIMING DOES NOT WORK

Although tempting, everyone knows at some level that market timing does not work.

You’ve heard me say many times, the problem with timing the market is that must be right twice. Exiting the market is usually the easy part.

The difficult part is deciding the opportune time to get back in.

The other issue with market timing is that the best days in the stock market come at the worst times.

For example, if you sold after every big down day – let’s say a 2% drop – and bought back in two weeks later when the coast is clear, you would’ve missed out on a third of gains over the past 20 years.

And even if you had the news headlines ahead of time, you would have no idea how the market would react.

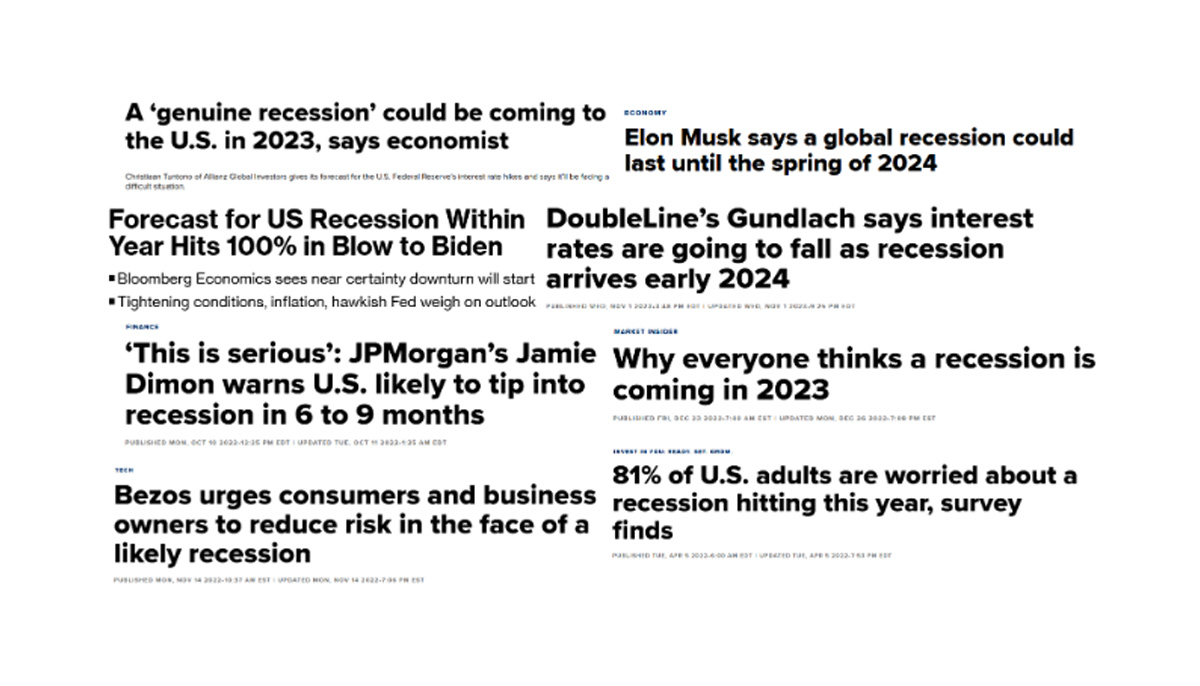

Here are the headlines going into 2023…

If you followed this advice, you would have missed out on two of the strongest years of market returns in recent history.

Remember long term returns are earned in volatile times, not when the market is going up and everyone is making money.

It’s when the world is panicking, and you have the fortitude to stick to the long-term plan.

THE MARKET IS NOT THE ECONOMY

Given the trade war is on our doorstep, Canadians feel particularly affected and rightly so given that it may have a significant effect on our economy.

That said, we need to separate the Canadian economy from your portfolio. They are related but they are not the same.

Your portfolio does not equal the Canadian economy and thus a pullback in the economy does not translate directly to a pullback in the investment strategy.

Only a portion of your portfolio is invested in Canadian companies and many of which may not be affected by the trade war.

We are global investors investing in companies all around the world.

DIVERSIFICATION IS YOUR FRIEND

So how do we navigate through this? Diversification.

As one portfolio manager put it – we’re not in the business of making binary bets.

When there is little visibility, we make sure we are diversified. So, when some things aren’t working, others are.

For example, while there is a lot of noise in the US and Canada, here are the returns in other parts of the world as of March 5th:

- Germany: +21%

- Italy: +19%

- France: +17%

- UK: + 12%

- China: +21%

As you can see, there are parts of the world and therefore parts of your portfolio that are working.

What about bonds?

In 2022 when we had soaring inflation, bonds provided no protection against a falling stock market.

That’s not the case so far in 2025.

The bond side (i.e., the more conservative side of your portfolio) is providing protection.

Beyond diversification, underneath the hood, there is a lot of activity.

The portfolio managers are making the necessary adjustments, rotating into different sectors, and continuing to search for companies on sale.

THIS TOO SHALL PASS

This is temporary.

I know every pullback and correction feels like the world is coming to an end, but it’s not.

If you’re a buy and hold investor (like we all are), this is a blip.

Looking back, do you even remember the 34% market drop in Covid? Or the 8% drop in August or the 6% drop in April?

Ask yourself if you plan to sell your portfolio in the next 3-6-12 months?

If not, then these market corrections do not matter.

What matters is that you have a plan that matches your risk tolerance and you’re able to stick to it. It’s the only way to reap the benefits.

The long-term remains undefeated….

The short term is always uncertain, and I suspect there is more bumpiness to come. However it’s important to remember, every correction is unique, but they all share one thing time in common – they end.

With that said, wish me luck – this is my first March break with the two kids at home.

This should be interesting…

On behalf of Surround Wealth Advisors,

Adil Mohammed, CFP®, CIM®, FCSI®

Wealth Advisor

Assante Financial Management Ltd.

Sources:

https://awealthofcommonsense.com/2025/03/is-international-diversification-finally-working/

https://www.theirrelevantinvestor.com/p/top-ten

https://surroundwealth.com/assante-market-update-expect-volatility/

The opinions expressed are those of the author and not necessarily those of Assante Financial Management Ltd. This material is provided for general information and the opinions expressed and information provided herein are subject to change without notice. Every effort has been made to compile this material from reliable sources however no warranty can be made as to its accuracy or completeness. Before acting on the information presented, please seek professional financial advice based on your personal circumstances.