The Surroundup

UNCERTAINTY IS THE PRICE OF ADMISSION

- by Adil Mohammed, CFP®, CIM®, FCSI®

- January 29, 2026

“The one who can tolerate the most uncertainty is the one who will eventually win.” — Sahil Bloom

By the time you’re reading this, per Larry David, the statute of limitations on saying Happy New Year will likely have expired — so let me send my best wishes for 2026!

Less than a month into the year, it already feels like we’ve had a year’s worth of headlines packed into three weeks. More on that shortly.

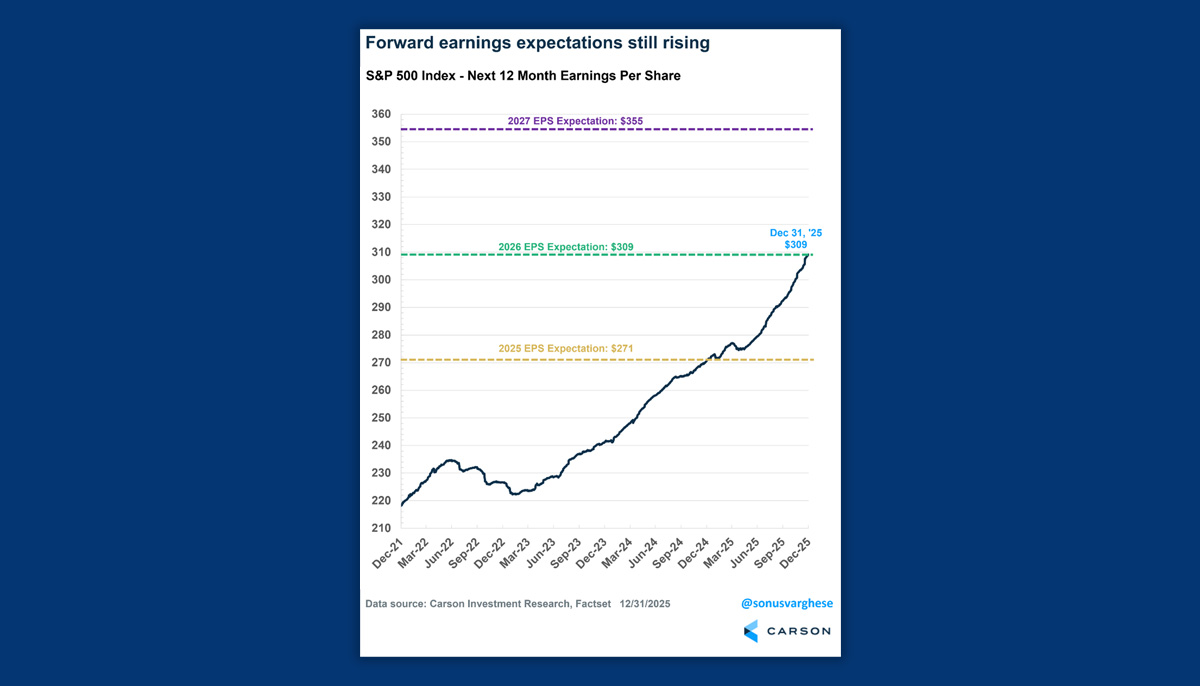

A Quick Look Back: 2025 in Review

If you missed it, here’s my full 2025 recap:

👉 https://surroundwealth.com/2025-thats-a-wrap/

The TL;DR: earnings drove the stock market in 2025.

Here are the numbers behind that statement.

Of the 17.9% total return in the U.S. stock market last year, 14.3% came directly from earnings growth. That distinction matters.

Of the 17.9% total return in the U.S. stock market last year, 14.3% came directly from earnings growth. That distinction matters.

Investors often hear about multiple expansion — which simply means investors are willing to pay a higher price for the same dollar of earnings. When returns are driven by multiple expansion, prices rise without companies necessarily becoming more profitable.

That wasn’t the case in 2025.

Multiple expansion played only a small role. The vast majority of returns came from companies actually earning more money.

Translation: businesses performed better — exactly what you want to see.

Most of the market’s gains were supported by real fundamentals, not speculation or hype.

This was not:

❌ Just inflated prices

❌ Just investors chasing momentum

❌ Just “multiple expansion mania”

It was:

✅ Companies earning more

✅ Profits justifying higher prices

Strong markets. Scary headlines. But earnings did the heavy lifting.

More Than Just the Magnificent 7

At this point, some of you may be thinking:

“Okay Adil — earnings drove the market… but wasn’t it really just the big tech names doing all the work?”

That was a fair concern in prior years.

In 2023 and 2024, much of the market’s performance was driven by a small group of mega-cap technology companies — often referred to as the Magnificent 7 (Apple, Microsoft, Alphabet/Google, Amazon, Nvidia, Meta/Facebook, and Tesla).

But 2025 looked very different

Last year, more than half of the market’s return came from the other 493 companies in the S&P 500. In other words, gains were no longer concentrated in just a handful of stocks — they were far more broadly distributed across sectors and industries.

That’s an important and encouraging shift.

Broad participation typically signals a healthier market, one that’s supported by a wider range of businesses, earnings streams, and economic activity — rather than being overly dependent on a few dominant names.

With that backdrop in mind, let’s turn our attention forward.

2026 Outlook: Déjà Vu?

“During the last 11 major geopolitical events, the S&P 500 was on average just 0.3% lower one week after the event and 7.7% higher twelve months later.” — UBS

I can’t help but feel like I’ve seen this movie before.

So far, 2026 looks like a continuation of 2025 — significant geopolitical developments, nonstop headlines, and a market that largely looks past the noise.

In just the first few weeks of the year, we’ve already seen:

- Week 1: A surprise overnight military operation involving Venezuela

- Week 2: Headlines around a Department of Justice investigation involving the Federal Reserve Chair

- Week 3: Tariff threats toward several EU countries tied to Greenland, along with speculation about potential military action

- Later that week: A rapid shift in tone at Davos (a.k.a TACO trade), with rhetoric softening and a “framework” emerging instead

- Week 4: New tariff threats directed at Canada in the context of China-related trade discussions

And that’s only a partial list.

Despite all of this — and despite how unsettling some of these headlines may feel — markets are sitting near all-time highs as I write this.

It’s a powerful reminder that while geopolitical events dominate the news cycle, they do not dictate long-term market outcomes.

If you can’t eliminate the noise, then separate it.

Why Investors Actually Need the Noise

Markets don’t rise despite uncertainty — they rise because of it.

As Sir John Templeton said:

“Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.”

Strong markets climb a wall of worry. When everything feels calm, obvious, and universally bullish, returns tend to stall — because there’s no new good news left to push prices higher.

Strong returns require:

- Doubt

- Disagreement

- Fear

History is clear:

- We don’t get a strong 2019 without the late-2018 selloff

- No 2021 recovery without the COVID crash

- No 2023–2024 without the 2022 bear market

- No 2025 without “Liberation Day” tariffs

Those downturns weren’t mistakes — they were the setup.

They reset valuations, flush out excess optimism, and create opportunities to buy great companies at better prices

No one enjoys them in the moment. But for long-term investors, they’re not a flaw in the system — they’re the feature.

If you want strong long-term returns, you have to accept — and expect — discomfort along the way.

The Setup for 2026

When you strip away the headlines, the message from market professionals is remarkably consistent: the fundamentals entering 2026 are constructive.

- Economic growth is expected to remain positive

- Interest rates are stable or trending lower

- Inflation is easing (even if uneven)

- Fiscal spending remains supportive

- Corporate earnings — the single most important long-term driver of markets — are expected to grow.

We’re also seeing healthier market leadership, with gains broadening beyond a handful of mega-cap stocks.

That said, expectations are not guarantees. There are always risks.

Markets never move in a straight line. Mid-term election years tend to be more volatile, pullbacks are normal, and surprises are inevitable.

In fact, markets decline around 14% in the average year, yet still finish positive roughly three-quarters of the time. Volatility isn’t a sign that something is wrong — it’s the price of admission.

Our job isn’t to avoid downturns. It’s to plan for them, survive them, and use them so portfolios are positioned to benefit when markets recover.

As Morgan Housel puts it, “Risk is what’s left over after you think you’ve thought of everything.” That’s why portfolios are built to be diversified, flexible, and resilient — not dependent on perfect forecasts or flawless timing.

Because in the end, the investors who do best aren’t the ones who try to jump in and out. They’re the ones who stay disciplined, stay invested, and keep their focus on the long term.

And that’s exactly how your plan is built.

Adil Mohammed,CFP®, CIM®, FCSI®

Wealth Advisor, CI Assante Wealth Management Ltd.

Mutual Fund Registered Advisor

The opinions expressed are those of the author and not necessarily those of CI Assante Wealth Management Ltd. This material is provided for general information and the opinions expressed and information provided herein are subject to change without notice. Every effort has been made to compile this material from reliable sources however no warranty can be made as to its accuracy or completeness. Before acting on the information presented, please seek professional financial advice based on your personal circumstances. CI Assante Wealth Management Ltd. is a Member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization.